Have Fun Without Worries! It's Tax Deductible!

What is entertainment for tax purposes?

Entertainment expenses include the cost of entertaining customers or employees at social events, clubhouse, restaurant, etc... which is also part of the sales function of many businesses.

The business owner may deduct 50 percent or 100 percent of certain entertainment expenses.

"Entertainment" includes the provision of:

✅ Food

✅ Drink

✅ Recreation or hospitality of any kind

✅ Accomodation or travel

in promoting or in connection with a trade or business carried on by that person.

The business owner may deduct 50% or 100% of certain qualifying entertainment expenses.

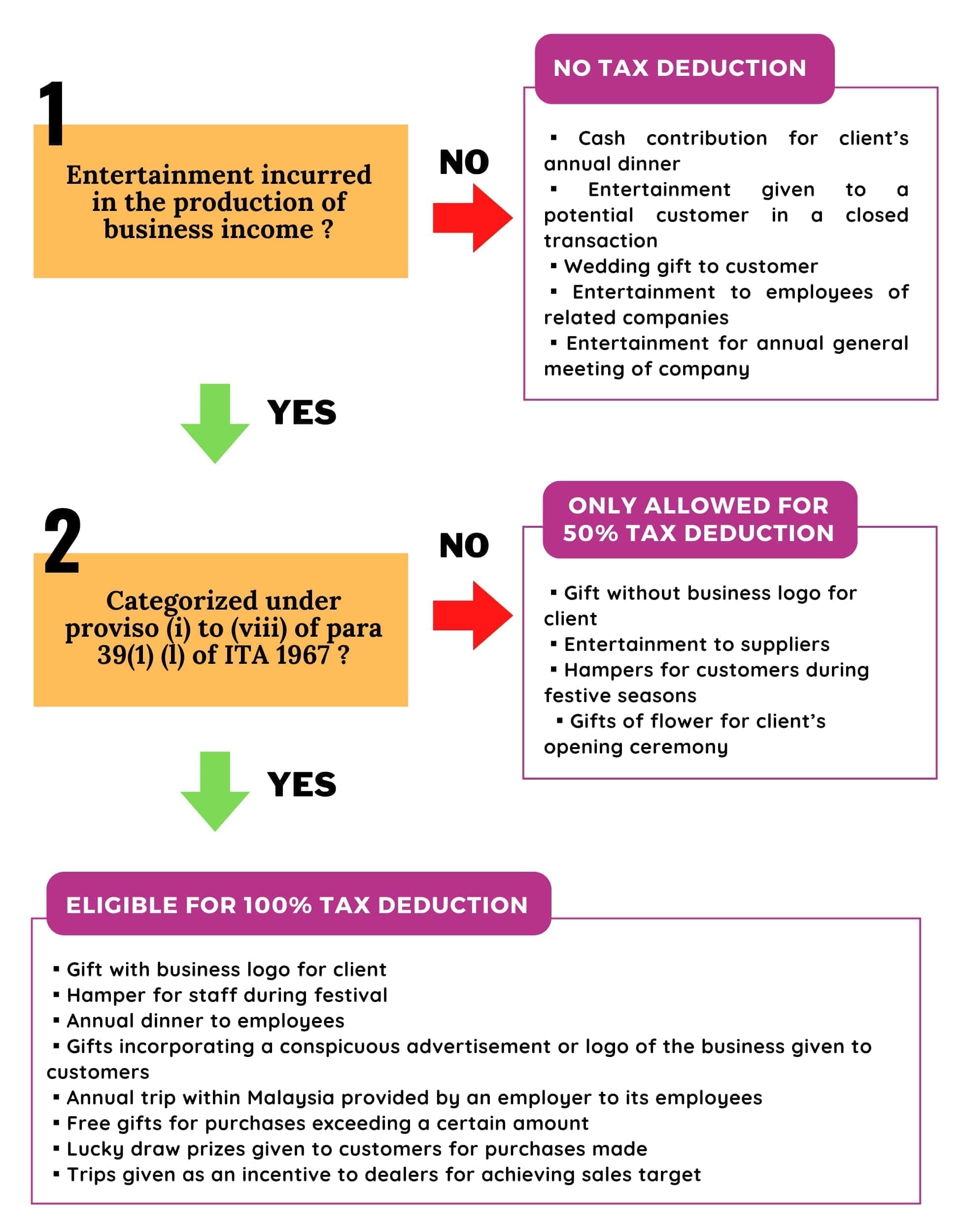

Steps to ascertain tax deduction on entertainment expenses

*In reference to Public Ruling No. 4/2015*

Principle of tax deduction on entertainment expenses

Section 18 of the ITA explains any food, drink, recreation or hospitality of any kind and accommodation or travel provided by a person or an employee of his, with or without consideration paid whether in cash or in kind, in promoting or in connection with a trade or business carried on by that person, would be treated as entertainment expenses.

Expenses which is wholly and exclusively incurred in the production of gross income will qualify for tax deduction under subsection 33 (1).

However, only entertainment expenses that are categorized specifically under proviso (i) to (viii) of paragraph 39 (1) (l) are fully allowed as a deduction against gross income. Otherwise, only fifty percent of such expenditure would be allowed for tax deduction.

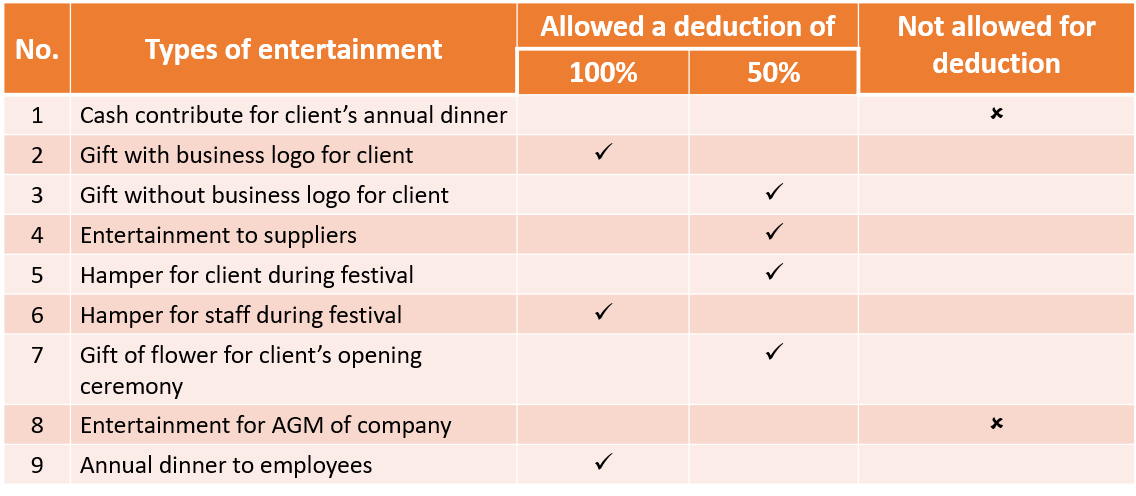

Types of Entertainment Expenses

*eligible for 50% and 100% tax deduction*

Home About Us Contact Us Site Map

Copyright 2025 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.