Service Tax - Intra Group Relief

Published: 2018

Background

To eliminate the tax cascading effect on taxable services provided within the same group of companies, it

is important for businesses to consider the eligibility of intra-group relief which is available for selected

taxable services under Group G (Professional Service) of First Schedule, Service Tax Regulation 2018.

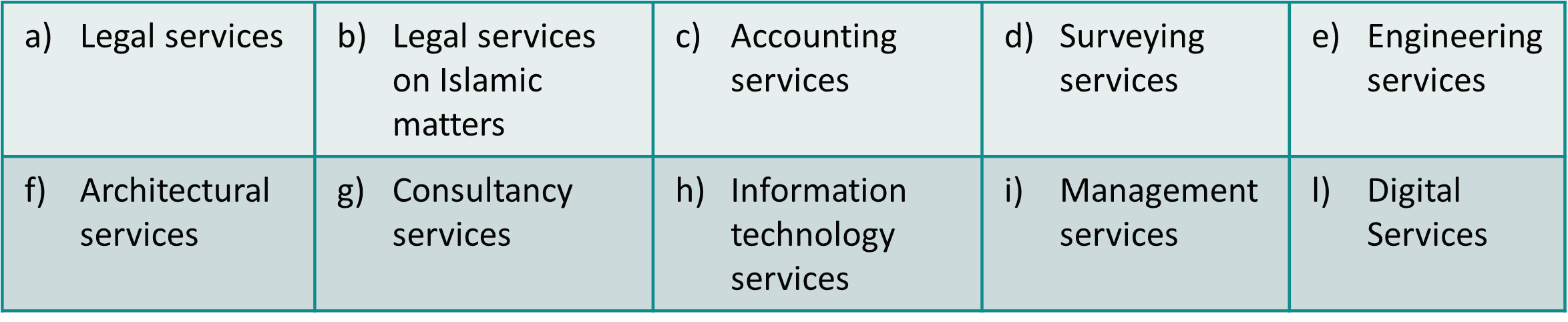

General Principle

In accordance with paragraph 3 of First Schedule, Service Tax Regulation 2018, where a company in a

group of companies provides any taxable service specified in item (a), (b), (c), (d), (e), (f), (g), (h), (i) or

(l) in column (2) in Group G to any company within the same group of companies, such service shall

not be a taxable service.

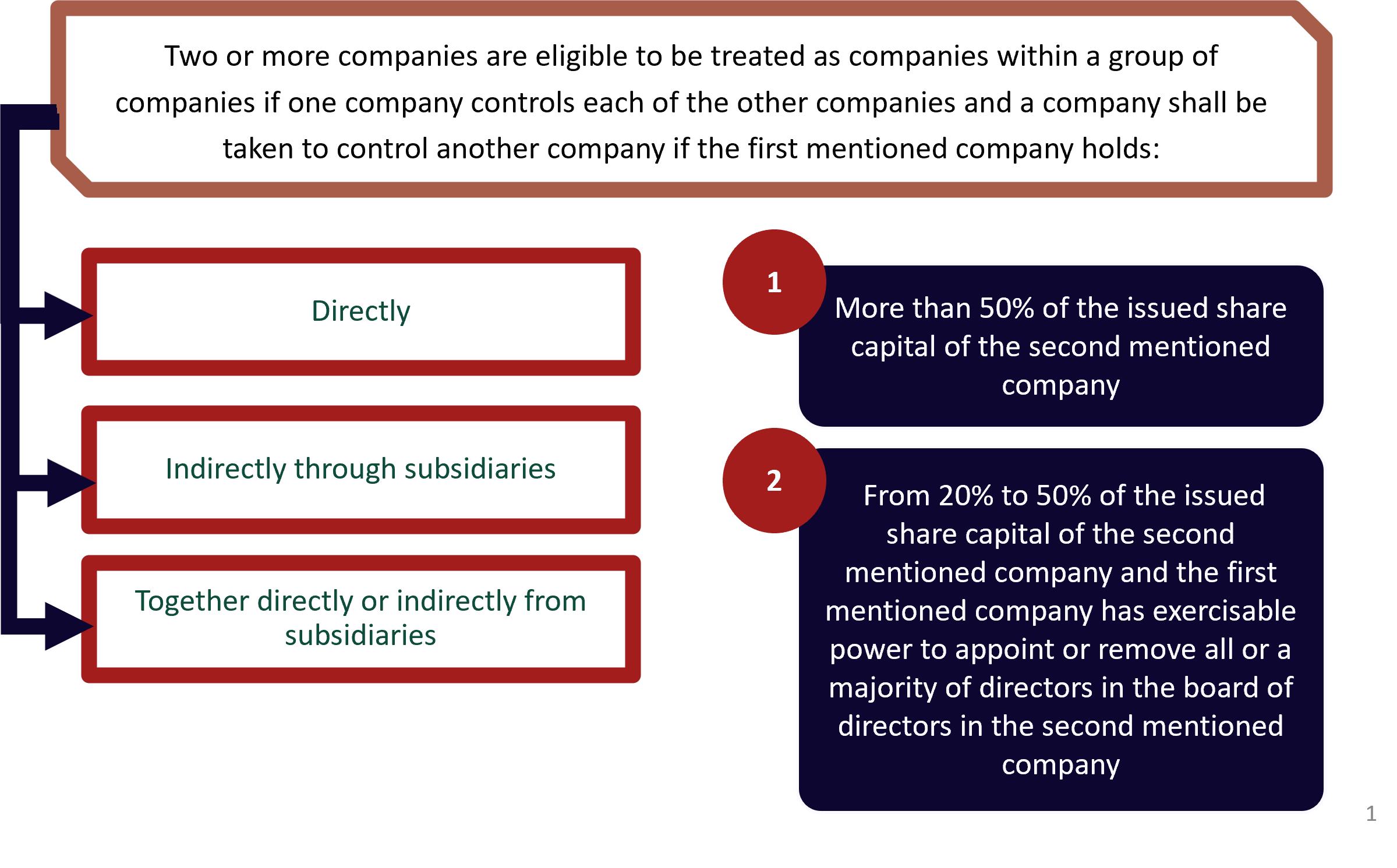

Definition of Companies Within Group of Companies

Timelines of Intra-Group Relief

Where a company provides the same services to another company outside the group of companies, such services provided to any company outside or within the group of companies shall be treated as a taxable service and subject to service tax.

Where a company in a group of companies acquires the same services from any company (other than foreign registered person) within the same group of companies outside Malaysia, such service shall not be an imported taxable service.

Where a company provides any taxable service to another person outside the group of companies, the same taxable service provided to any company outside or within the group of companies shall be a taxable service if the value of services provided to a third party exceeds 5% of the total value of services provided by the company within 12 months (the 5% Rule). However, this rule does not apply to imported taxable services acquired from the group member located outside Malaysia.

Where a company who is a foreign service provider (FSP) or foreign registered person (FRP) provides any digital service to any company in Malaysia within the same group of companies with the FSP or FRP, such digital service shall not be subject to service tax.

If the FSP or FRP provides the same services to another company outside the group of companies, such services provided to any company outside or within the group of companies shall be treated as a taxable service and subject to service tax. The 5% rule is not applicable for FSP or FRP who provides digital service.

Method of Calculation of The Twelve (12) Months Under 5% Rule

The 12-month period is based on future method.

Where it cannot be ascertained that total value of taxable services to third parties will not exceed the 5% threshold, service tax shall be charged on the taxable services provided to group members.

Example for 5% Rule

Bright Star Sdn Bhd provides IT service & Management Service to the company within the same group of the companies and third party:

* 5% rule should be calculated based on each type of taxable services

- IT service provided by Bright Star Sdn Bhd to the company within the group of companies is entitled for the group relief

- Management service provided by Bright Star Sdn Bhd to the company within the group ofcompanies and the third party is not entitled for the group relief.

Home About Us Contact Us Site Map

Copyright 2025 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.